A new regime for reviewing investments, mergers and acquisitions

The National Security and Investment Act 2021 (NSIA) comes into force on 4 January 2022 creating a new standalone regime giving the UK Government greater power to scrutinise – and potentially intervene – in acquisitions and investments on the grounds of protecting national security.

This new UK regime replaces the national security aspects of the UK Government’s intervention powers under the Enterprise Act 2002. The substantive provisions come into force in January, but it gives the UK Government retroactive powers to call in for review any qualifying transaction which completed after 12 November 2020 for up to five years from 4 January 2022.

The scope of the NSIA is broad and the consequences of non-compliance are significant. Failure to notify and obtain approval where required renders the transaction void and subjects the acquirer to financial and criminal sanctions.

The UK Government estimates that the new regime will result in between 1,000 and 1,800 notifications, and around 100 “called-in” transactions, per year, although some commentators believe that these are underestimates. Blocking of transactions by the UK Government is expected to be rare, with remedies – anticipated to impact around 10 deals per year – more likely to involve conditions being imposed on the acquisition or investment.

What transactions fall within the scope of the NSIA?

The NSIA establishes both a mandatory and voluntary notification regime targeting 17 specific industry sectors (outlined in the table below) where there could be a national security implication.

The UK government has published regulations containing detailed definitions of what it considers to fall within each of these sectors (though rather unhelpfully has not defined what is meant by “national security”).

There are no minimum turnover or share of supply thresholds for notification and no exemptions for small transactions.

The regime also applies to both UK and non-UK acquisitions and investments, with the focus on the location and nature of the underlying business or asset being acquired, not on the jurisdiction(s) where the acquirer and its controllers are based. Accordingly, acquisitions may be caught even where the buyer / investor is based and controlled in the UK or in the case of intra-group reorganisations. Conversely, acquisitions involving a non-UK target might also be caught if it has subsidiaries or carries on any business in the UK in any of the 17 sectors.

Notification processes

- Mandatory notification

The mandatory notification regime applies to acquisitions in any of the 17 sectors where the following threshold of voting rights are acquired (in essence, share acquisitions, including increases in current holdings): >25%; >50%; >75%; or voting rights that enable or prevent the passage of any class of resolution in qualifying entities.

Failure to notify by the acquirer or the investor will render the transaction void and could also give rise to financial penalties (£10m or 5% of global turnover – whichever is greater) and criminal penalties (up to five years’ imprisonment for the acquirer’s directors).

2. Voluntary notification

The voluntary notification regime and the ability for the Secretary of State to call-in a transaction applies to both qualifying share and qualifying asset acquisitions. A qualifying asset is not limited to acquiring an entire business. It also includes land, tangible moveable property and certain IP and would be likely to fall within the regime if the asset is used by a UK person or a non-UK person to supply to the UK.

Parties can also notify a transaction to the Secretary of State voluntarily if it involves an acquisition of material influence (which in certain circumstances could be seen as only 15% of voting rights). This may be a preferred option for parties as it gives legal certainty and avoids a risk that the transaction be ‘called-in’ by the Secretary of State post-completion.

3. Notification process and timing

The timing for processing notifications is stated to be 30 working days to assess the notification, plus a further 30 working days (that could be extended to 45 working days) to undertake the national security assessment. Our experience to date is that the initial 30 working day period is being adhered to which is encouraging from a deal timing perspective.

Unlike in the case of competition clearance notifications, NSIA notifications will be confidential. Only notices of final orders made by the UK Government will be published, with sensitive information removed.

Parties can seek advice from the newly formed Investment Security Unit (ISU) for informal guidance on the implications of the regime for a particular transaction before submitting a notification. In practice, where there is any doubt as to whether the NSIA applies, the parties will often make the decision to make a notification in order to start the clock ticking rather than further delay waiting for a response from the ISU.

The notification form is submitted via the ISU’s online portal using a prescribed form where various information is required to be uploaded about the relevant entity’s business that falls within

4. Secretary of State call-in powers

The NSIA notification requirements are combined with a broad power enabling the Secretary of State to call in transactions that may present a risk to UK national security for up to six months from becoming aware of the transaction. This is subject to a longstop of five years after completion (although this does not apply to transactions which require mandatory notification).

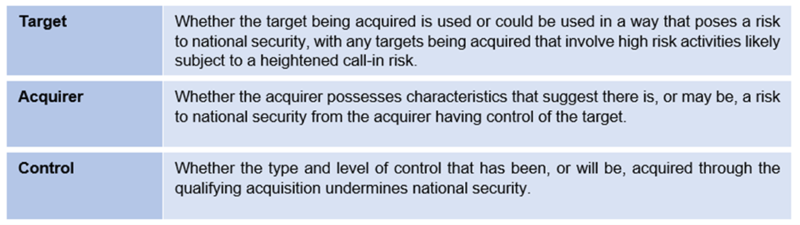

The UK Government’s likely approach to exercising its call-in power will be to consider the following risk factors:

Key considerations for acquirers and investors

- Regular investors and serial acquirers will need to adopt strategies for evaluating and negotiating transactions.

- Parties should seek to allocate and mitigate risks associated with the NSIA in their deal documentation.

- Parties should consider in due diligence whether the proposed transaction will be within the scope of the NSIA regime and what approach should be taken.

- Parties can seek to prepare by compiling the required information on their corporate structure and ownership so they can submit the notification form via the ISU online portal in a timely manner. This may be a more involved process for private equity and venture capital funds due to the nature of how they are typically controlled.

- In respect of mandatory notifications, unless parties are content to pre-notify ahead of signing, transaction documentation will likely need to be structured in a split exchange and completion fashion rather than a simultaneous closing.

- Where notification is voluntary, the parties will need to evaluate the risks of the likelihood of the transaction being called-in. They can be mitigated by either seeking guidance informally from the ISU prior to completion and / or starting the clock on the six-month period by publishing details of the deal immediately post-completion to make the Secretary of State “aware” (though the NSIA does not yet prescribe what will constitute awareness for this purpose).

- Parties will need to be mindful of the potential extra-territorial application of the NSIA to their acquisitions where the acquired group carries on activities in the UK even if the entity being acquired is not established in the UK.

Authors

Follow us online