Online property lender LendInvest recently confirmed it is considering an initial public offering as one of a range of strategic options for the business”, adding its name to a list of rumoured IPO candidates that includes Zopa, RateSetter and Tandem Bank.

With 2019 expected to see a surge of public fintech issuance, the question to be asked is: why? After all, there is no shortage of appetite for fintech assets from private investors, with a record $3.3bn of private money invested into UK fintechs in 2018.

Credibility

For some fintechs, the appeal lies in the credibility and profile imparted by a public listing. For all the market commentary about mistrust of high street banks, the reality remains that established financial institutions have certain advantages in the areas of trust and security, supported by long track records. For consumer facing fintechs such as LendInvest, an IPO is seen as providing a short cut to gaining public trust.

“Being on the London Stock Exchange is the ultimate badge of a grown-up business” says Christian Faes, CEO and Co-Founder of LendInvest.

For peer to peer lending platform Raize, a public listing was a marketing strategy, more than it was a fundraising strategy. The startup competes “on a daily basis” with banks and credit institutions, and wanted to get the message out that Raize is a serious player.

“One of the main motivations for the IPO was to raise the profile of our company and give it a more institutional spin, releasing it from the startup image it had so that more people would be comfortable working with us” says José Maria Rego, co-founder of Raize.

Permanent capital

Other fintechs cite the cost and permanence of capital as the attraction. Whilst venture capital investment in fintech continues to grow, a key advantage of public equity lies in the long-term nature of the investment as opposed to the usual seven to ten-year fund horizon that has been the norm in the private equity industry.

A higher degree of permanent capital allows businesses to access opportunities for longer time-periods, acquire assets at attractive valuations when rivals are unable to do so due to unfavourable market conditions or internal distress and, most importantly, ride out periods of high market volatility – a valuable commodity for lending platforms or digital wealth managers yet to experience a prolonged economic downturn.

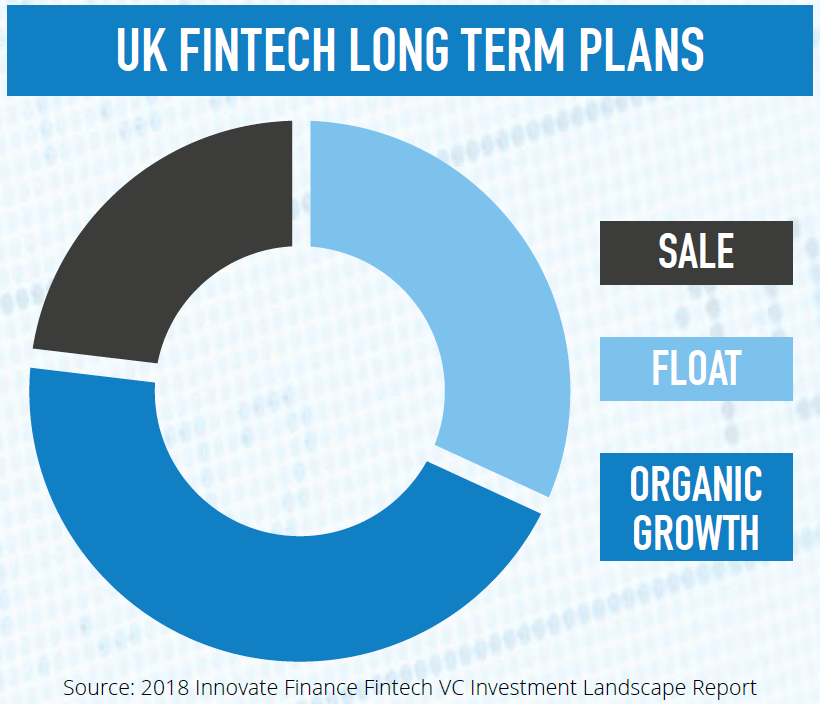

Release equity for stakeholders

Although recent years have witnessed a growing number of fintech M&A deals such as PayPal’s 2018 acquisition of iZettle, appetite for M&A amongst FinTech founders is more limited with only 23 per cent of UK fintechs citing a sale as part of their long term plan versus 43 per cent who are focusing on organic growth.

With many fintech founders focusing on organic growth instead of exit opportunities, an IPO can provide a valuable mechanism for early investors to release equity, whilst allowing management to maintain day to day control of the business.

The recent £2.15bn IPO of payment provider Network International on the Main Market of the London Stock Exchange is an interesting, if extreme illustration of this: the company raised no new money in the float whilst the selling shareholders receiving gross proceeds of approximately £1bn.

Examples such as this are, of course, somewhat uncommon with new investors typically preferring to finance growth instead of providing an exit to shareholders but do provide a useful example as to how a listing can be used to balance the interests of different stakeholders.

Maintain strategic control

One concern that commonly arises when discussing any capital raising – whether in the form of venture capital, corporate investment or public equity- is the question of control, with management teams commonly unwilling to cede strategic control.

In the private arena, where we frequently advise fintech businesses, this concern frequently manifests itself in lengthy negotiations with investors over what contractual restrictions should apply to a company’s day-to-day operations. In the public markets, we have seen a growing use in the US at least of dual class shares with differing voting rights, which provide management or founders with enhanced voting rights, as used by Lyft and Facebook.

Whilst dual class share arrangements are possible on the London markets, such arrangements are uncommon, in part because of understandable investor resistance to such arrangements but also because, in many cases, there is simply no need: the diverse nature of a public company’s shareholder register and lack of contractual restrictions imposed by private investors mean that management teams with minority holdings frequently maintain strategic control of the business post IPO notwithstanding any sell down.

Choosing a market

Whilst large cap floats such as Funding Circle’s 2018 debut on the Main Market of the London Stock Exchange attract the most public commentary, for companies at an earlier stage of their life cycle, AIM continues to be an attractive venue for high-growth tech businesses, accounting for 17 out of 42 IPOs or 40 per cent of all public debuts on the London markets in 2018. Despite the difficult political climate, AIM remains the most successful growth market, satisfying the needs of smaller, growing companies that either don’t meet the formal criteria for a Main Market or Nasdaq listing or, more commonly, are of insufficient scale to attract investor interest or research coverage on the US markets.

AIM tends to be comfortable with companies that have smaller annual revenue and market capitalisations, with many companies coming to AIM having an initial market capitalisation in the £30- 200m range – well below the level at which a Main Market or Nasdaq listing would be viable. At Fox Williams, we have in-depth experience of advising businesses that are planning an AIM IPO or considering whether this is their best next step.

Final thoughts

Whilst private equity and venture capital are likely to continue to dominate the fintech investment landscape for the foreseeable future, as the industry matures, we expect to see a growing number of businesses seeking to access the public markets. And whilst short-term fluctuations in share price will, no doubt, provide plentiful material for online commentators to trawl over, the success or otherwise of an IPO will take somewhat longer to play out.

Guy Morgan, corporate partner at Fox Williams advises organisations in the fintech space seeking to raise funding, whether by way of the public markets or through private equity/venture capital.

This article first appeared in the AltFi special report, May 2019. Download the PDF copy here.