Disagreements between shareholders and/or founders in a fast-growing start-up are often unavoidable. When they do arise, they can throw up emotive issues and a whole host of complex legal issues too.

The differing “hats” worn by the characters (shareholder/ employee/ director/ consultant) can be further complicated in family companies, where there are often long standing resentments added to the mix.

Due to the cost-of-living crisis and the stress it can put on business owners, we have seen an upturn in client enquiries about how to resolve shareholder fallouts. These enquiries range from clients at the start of a dispute to shareholders who have already agreed outline terms to settle their differences but are now trying to work out how these can work legally.

Using an illustrative example, we have provided a handy guide to solving your shareholder dispute.

The scenario

Two 50/50 shareholders in a UK private company in the travel industry (“TravelCo”) have a spectacular fallout. After months of painful negotiations, Shareholder A has agreed terms to purchase Shareholder B’s entire shareholding in TravelCo. However, Shareholder A has none of their own money and picks up the phone to instruct Fox Williams as follows:

“We have managed to settle our differences”

“TravelCo is going to buy back Shareholder B’s shares as I haven’t got any available funds”

“TravelCo also doesn’t have sufficient cash flow to purchase them all on day one, so we’ve agreed a three-year payment plan”

“Can you draw up the documentation to make all this happen?”

The hurdles to overcome

The short answer to the question above is yes, but the execution is more complex.

There is the small issue of the Companies Act 2006 (the “Companies Act”). The Companies Act provides that payment for a share buy back must be made by the company in full at completion. This means that deferred consideration for a buy back is not permitted (and advance payments are also unlikely to be acceptable). Therefore, the following must be considered:

- the structure to be put in place which allows for the commercial intent (i.e. TravelCo’s funds being used over a period of time to buy back the shares) without falling foul of the Companies Act; and

- the terms for the continuing, as well as the exiting shareholder, and the documentation needed to achieve this.

This could be accomplished in one of two ways:

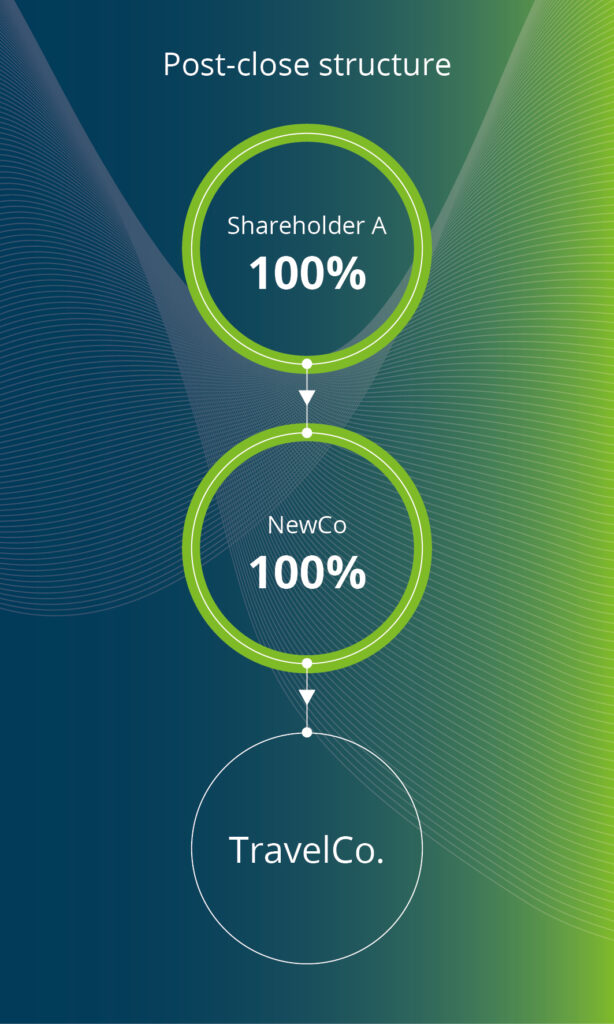

Structure 1 – use of a NewCo

In the simplest of terms, a NewCo is established by Shareholder A. NewCo makes an offer to buy all of Shareholder B’s shares in TravelCo in exchange for deferred cash consideration. At the same time, NewCo will often also make an offer to Shareholder A to buy their shares in TravelCo in exchange for the issuance of shares in NewCo.

There is no buy back by TravelCo (as NewCo is the purchaser paying deferred consideration to Shareholder B) so there is no problem under the Companies Act.

Pre-closing structure:

Post-close structure:

Considerations for Shareholder A

The main issue here is tax. Clearance should be sought from HMRC to ensure, amongst other things, that no capital gains tax is payable by Shareholder A.

Advice will also need to be sought on stamp duty. Although this will be payable (albeit at 0.5%) on the cash consideration payable to Shareholder B, advice will be needed to ascertain if stamp duty can be avoided on the share for share exchange involving Shareholder A.

Considerations for Shareholder B

Here, all the shares are being transferred on day 1 and Shareholder B will have little, if any, assurance that they will be paid the deferred consideration. This is why a share charge over the capital of TravelCo will often be sought by Shareholder B in this scenario.

Also, Shareholder B will consider asking for other contractual protections such as information rights in relation to TravelCo’s affairs and / or consent matters over the operation of TravelCo going forward until all the deferred consideration is paid.

Documents required

As well as the Share Sale/Exchange Agreement and any security document relating to the share charge, there will also be the need for a settlement agreement which will include clauses such as:

- Waiver of all rights by all the parties.

- Restrictive covenants from Shareholder B.

- Assignment of any intellectual property rights by Shareholder B.

- Agreed position on confidentiality / announcements / references.

Structure 2 – buy back in tranches

In this structure, there are a series of share buy backs by TravelCo. There will usually be one umbrella sale agreement (the “Sale Agreement”) where there is an obligation on TravelCo to purchase and on Shareholder B to sell their shares over an agreed period of time. This is considered future, rather than deferred, consideration.

The price, sale dates and number of shares in each tranche are all agreed in advance. There is no issue with deferred consideration and the Companies Act as on each agreed completion date, there will be a pre-signed stock transfer form and all consideration applicable to that tranche of shares is fully paid. The Sale Agreement will also contain key terms to deal with events of default; grace periods and default interest.

Part 18 of the Companies Act 2006 sets out the procedure that must be followed to action a share buy back. Failure to comply to the Companies Act procedure could render the transaction void and will constitute a statutory offence by the company and every officer in default so it’s important to get it right.

We also recommend the seller seeks personal tax advice before making the buy back.

Considerations for Shareholder A

This will see Shareholder B continuing as a co-shareholder and usually as a director for some time until the final tranche of shares is bought back, so there is no clean break.

Shareholder A will want a clear mandate to run TravelCo to allow it to fund the future consideration, they will also want a clear understanding of Shareholder B’s role (or lack thereof!) going forward.

Considerations for Shareholder B

Pretty much the same as with a Newco structure. However, in addition, they will need to be careful to make sure that they don’t jeopardise any business asset disposal relief. This will typically see them wanting to remain as a director of TravelCo until the final tranche sale of shares. There will also need to be consideration given to the sale percentages so that, for example, on the final sale they are not selling only 2% of TravelCo’s capital (which is lower than the disposal percentage required to qualify for the tax relief).

Required documents

These would be very similar to Structure 1, except that there will be a series of future stock transfer forms needed with stamp duty payable on each buy back.

Travel regulations to keep in mind

For regulated travel businesses, another key consideration will be determining whether the proposed structure will result in a change of control event which will require consent from the relevant regulatory bodies (i.e. the Civil Aviation Authority (CAA), the International Air Transport Association (IATA), the Association of British Travel Agents (ABTA) and any other international regulators that regulate TravelCo). Each regulator has their own notification process and timeline to comply with and, depending on the circumstances of the transaction, the regulators may require certain financial information to be provided or they may want to review legal documentation such as the share buyback agreement.

Practical lessons to bear in mind

- If you are feeling exhausted and frustrated in the middle of a shareholder dispute, the other side are also likely to be in the same position.

- It is often said but usually true that a sensible deal is where both sides feel they have lost as they need to make material concessions to bridge the gap (usually on valuation of the shares).

- With some creative structural thinking, it is often possible to bring disparate positions closer together by the use of deferred consideration; security; tax allowances etc.

- Be aware of any regulatory consents required and their impact on timing.

- Avoid litigation if at all possible – it is costly and very stressful!

Contact us

Fox Williams has extensive experience in handling shareholder disputes and is aware of the tensions/acrimony which can arise in such circumstances.

If you have any questions about these issues in relation to your own organisation, please contact a member of the team or speak with your usual Fox Williams contact.

Authors

Follow us online